From policy document to cited calculation, in minutes.

ParaplanAI extracts the key figures from your policy documents and turns them into HMRC-cited tax calculations — in minutes.

77 HMRC worked examples · 0p tolerance · UK-hosted

Upload. Extract. Done.

Upload a provider statement, P60, DB or DC annual statement, or a bond chargeable-event certificate. ParaplanAI reads the figures off it; you confirm the few it flags. No re-keying — and what comes out is a document for the file, not just a number.

Reading and keying a provider statement by hand is the best part of 20 minutes. ParaplanAI does it in under a minute — you confirm the figures it flags.

Plan Information Research Pack — included.

Confirm the extracted fields once and the same facts produce a firm-branded Plan Information Research Pack — a plain-English summary of the policy facts you can save to the file, attach to a client, and export as PDF or Word. The same confirmed facts also feed the deterministic calculation — no second upload, no re-keying.

- Editable Word document and a PDF

- Firm-branded — your cover, headers and disclaimer

- Every unconfirmed field flagged

- Confirm once — no re-keying

Speak to us on 0306 999 0200 (8am to 6pm, Monday to Friday)Visit us at aldermere.co.uk

Calling from abroad? (+44) 306 999 0211

24 KINGFISHER COURT

HARWELL DRIVE

LEEDS

WESTGATE PARK

LS12 4QB

Dear Sir or Madam

Thank you for your recent enquiry. Please find enclosed the following:

- A current valuation

- Plan information

- Projection(s)

- Plan valuation

We are unable to send a response by e-mail as this isn’t a secure method of communication. The Origo Options pension transfer service supports the transfer of this plan, please ensure you quote all the relevant plan numbers on the Origo Options portal. Please accept this letter as confirmation that we do offer the uncrystallised funds pension lump sum (UFPLS) option.

If you need more information or have any questions, please contact us and we’ll be happy to help. So that we can deal with your queries quickly and efficiently, please quote the reference shown at the top of this letter.

Illustrative mock. Aldermere Assurance, Castlepoint Group, Meridian Wealth and all names, references and figures shown are fictitious and for demonstration only.

Choose a calculation, run the figures.

Choose your calculation, run it on the confirmed figures, and save it to the file.

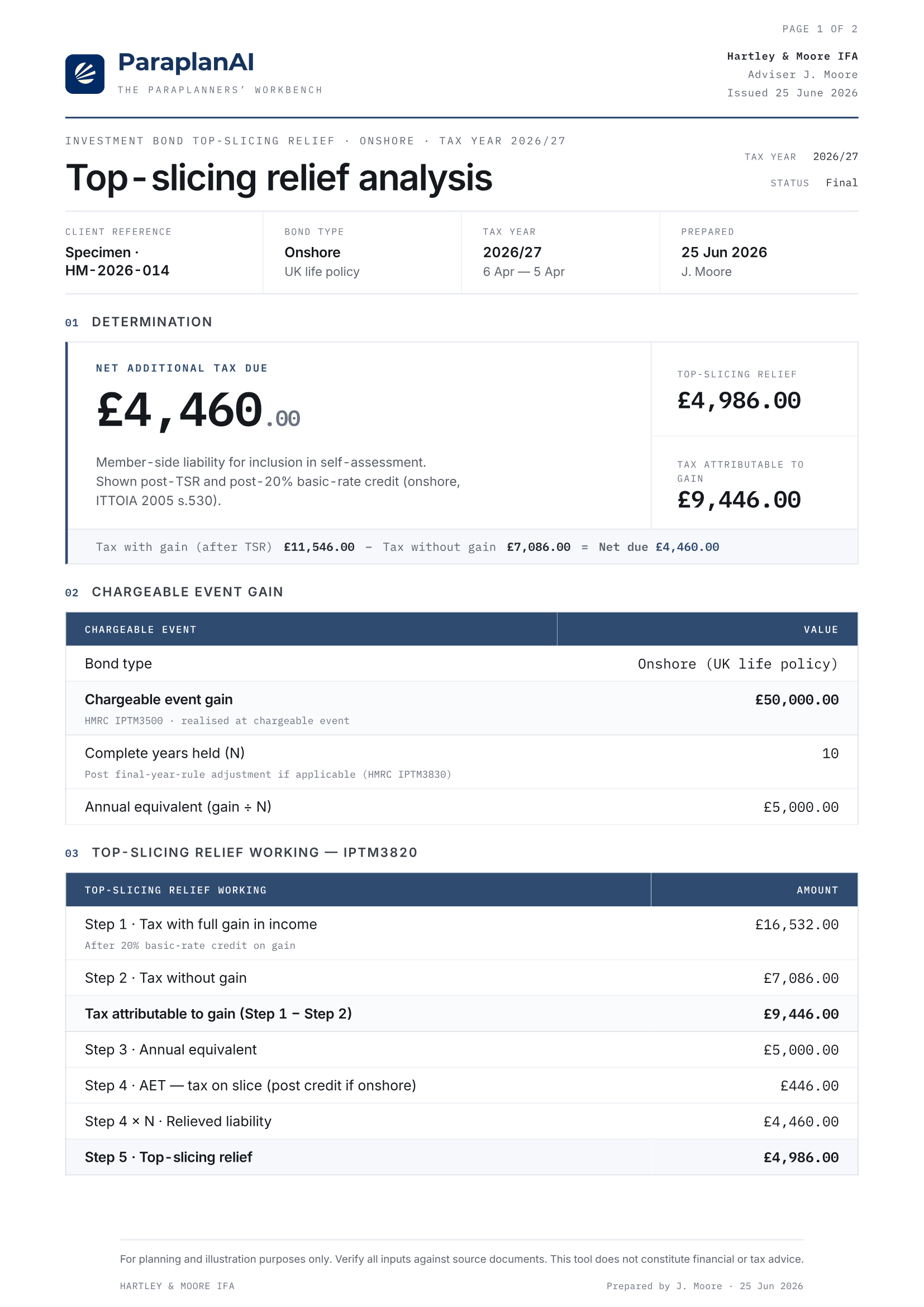

Lump Sum Allowance, TTFAC, top-slicing relief, annual allowance and carry-forward — pick one, run it on the figures you confirmed, and save the calculation to the client file. The AI reads the documents; it never does the maths. You can run a real case on the bond calculator now, with no sign-up.

Every figure, traced back to the manual.

Every figure is calculated in code against HMRC's published rules and checked to the penny against HMRC's own worked examples. Each calculation is assembled from named HMRC sources — IPTM3820, PTM057100, PTM055100, PTM171000 — and the result carries the citation back, including the post-2021/22 PSA recalculation (IPTM3820 / HMRC Agent Update 83 (2021)) that many tools still haven't updated. Run the same case on the bond calculator with no sign-up, or read the corpus at /trust.

The time it takes back.

Move the sliders to your own caseload. The estimate uses the lower bound of industry-reported ranges and rounds the saving down — a figure you can stand behind, not a best case.

£500.00 a month

≈ 10 hours a month · ParaplanAI Pro (£69.00/month) pays for itself the first month

Illustrative — based on industry-reported ranges, using the lower bound of each and rounding savings down. How this is worked out.

The output is a document you can file.

Every run produces a PDF like this.

The figure on the left is the engine's own regression case — the same arithmetic the annex carries, to the penny.

- The figure, and the working behind it

- The HMRC reference each step is built on

- Your firm branding, cover and disclaimer

- A version stamp — replayable six years on

Per user, per month.

Common questions.

Where does the calculation come from?

Each calc cites the relevant HMRC PTM/IPTM paragraph and the underlying statute. The engine carries a version stamp; saved scenarios remain reproducible against the version they were signed under.

Is ParaplanAI giving regulated advice?

No. ParaplanAI is a calculation and reporting tool used by the regulated adviser. It produces the figure and the working — recommendation and suitability remain yours.

What about client data?

Uploaded source documents are deleted within 24 hours of upload; only the figures you confirm are kept. You control retention — delete any client, policy or calculation in one click, and finalised calculations are kept only for the window your firm sets (six years by default). All data is held in encrypted UK databases on UK-only infrastructure.

Can I use my own PDF template?

On the Firm plan. Upload your firm cover sheet, headers, signature blocks and disclaimer; calculation data populates from the scan. Up to 5 templates per firm.

What about the tax-year change?

Statutory inputs for the new tax year are loaded as draft from the moment HMRC publishes them and confirmed within 48 hours. Old scenarios show a banner if the rules change.

How long does onboarding take?

A short walkthrough, then run a real case with your own figures. Most teams put through a first live calculation the same day.

Run a real case end to end.

Run a real bond case on the calculator now, with no sign-up — or start free and put a first case through end to end.